Mergers and Acquisitions

Mergers and Acquisitions

An organization may grow its operations either by internal expansion or by expanding externally. In the case of internal expansion, the organization grows gradually over time in the normal course of its operation, through acquisition of new assets, advancement of technology, replacement of the technologically obsolete equipments, and addition of the new lines of products. On the other hand in case of external expansion, the organization acquires either a running organization or a unit of the running organization and grows overnight through corporate combinations. These combinations are in the form of mergers, acquisitions, amalgamations, and takeovers and have become important features of organizational restructuring. These combinations play an important role in the external growth of the organization. Besides the external growth, these combinations also take place because of the marketing strategy of the organization.

Mergers and acquisitions (M&A) is a general term which is used for the consolidation of organizations or the assets. The terms ?merger? and ?acquisition? are often uttered in the same breath and are used as though they are synonymous, but both of these terms mean slightly different things. Over the past decade, M&A have reached unprecedented levels as organizations use corporate financing strategies to maximize shareholder value and create a competitive advantage.

?One plus one makes three? is the equation and the special alchemy of a merger or an acquisition. The key principle behind taking over another organization is to create shareholder value over and above that of the sum of the two organizations. Two organizations together are more valuable than two separate organizations. This is the main reasoning behind M&A.

This rationale is particularly attractive to organizations when times are tough. Strong organization acts to take over other organizations to create a more competitive, cost-efficient organization. The organizations come together in the hope to gain a greater market share or to achieve greater efficiency. Because of these potential benefits, target organizations often agree to be taken over when they know they cannot survive alone.

Mergers and acquisitions are complex and involve many parties. They involve many issues which include (i) corporate governance, (ii) form of payment, (iii) legal issues, (iv) contractual issues, and (v) regulatory approvals. M&A also requires application of the valuation tools for the evaluation of the M&A decision.

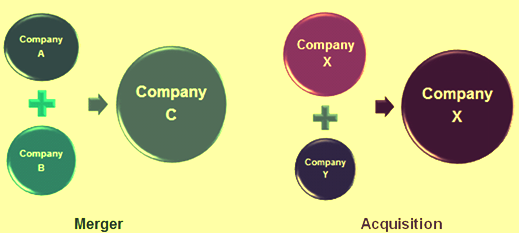

There are several types of transactions classified under the concept of M&A. A merger happens when two organizations, often of about the same size, agree to go forward as a single new organization rather than remain separately owned and operated. In case of an acquisition there is a take-over of one organization by another organization in which no new organization is formed. From a legal point of view the organization which has been taken over ceases to exist and the buyer organization swallows the total operations of the taken over organization. The concept of M&A is shown in Fig 1.

Fig 1 Concept of M&A

According to Straub the phrase M&A refers to ?the aspect of corporate strategy, corporate finance, and management dealing with the buying, selling, and the combination of another company that can aid, finance, or help a growing company in a given industry to grow rapidly without having to create another business entity, i.e. when a company engages in M&A activity and decides to acquire a target company it is making an investment?. The general principle is that the acquiring organization is to go ahead with the acquisition if by doing so it creates a net contribution to shareholders wealth.

Types of M&A

M&A can take place (i) by purchasing assets, (ii) by purchasing common shares, (iii) by exchange of shares for assets, and (iv) by exchanging shares for shares. M&A can take two forms namely (i) merger through absorption, or (ii) merger through consolidation. Based on an economic perspective depending on the business combinations, whether in the same industry or not as well as based on the perspective of structuring of the operations, there are several types of mergers which take place between the organizations. A few types, distinguished by the relationship between the two organizations which are merging are as follows.

- Horizontal merger – In the horizontal merger it takes place between two organizations which are in direct competition and share the same product lines and markets.

- Vertical merger ? It takes place between an organization and with its supplier or customer.

- Market extension merger – Under this type of merger, merger takes place between two organizations which sell the same products in different markets.

- Product extension merger – Under this type of merger, merger takes place between two organizations which sell different but related products in the same market.

- Conglomeration – Under this type of merger, merger takes place between the two organizations which have no common business areas.

There are two types of mergers which are distinguished by how the merger is financed. Each has certain implications for the organizations involved and for investors. These are given below.

- Purchase mergers – As the name suggests, this kind of merger occurs when one organization purchases another. The purchase is made with cash or through the issue of some kind of debt instrument. In this type of merger, the acquiring organization often prefers this type of merger since it can provide it with some tax benefits. Acquired assets can be written-up to the actual purchase price, and the difference between the book value and the purchase price of the assets can depreciate annually, reducing taxes payable by the acquiring organization.

- Consolidation mergers – With this merger, a brand new organization is formed and both the organizations are brought into and combined under the new entity. The tax terms are the same as those of a purchase merger.

From a legal perspective, there are different types of mergers like short form merger, statutory merger, subsidiary merger and merger of equals.

In case of an acquisition, the issues involved may be only slightly different from a merger. In fact, it may be different in name only. Like mergers, acquisitions are actions through which organizations seek economies of scale, efficiencies and enhanced market visibility. Unlike all mergers, all acquisitions involve one organization purchasing another and hence there is no exchange of stock or consolidation as a new organization. Acquisitions are either congenial when all the parties feel satisfied with the deal or are hostile.

In an acquisition, as in some of the merger deals, an organization can acquire another organization with cash, stock or a combination of the two. Another possibility, which is common in smaller deals, is for one organization to acquire all the assets of another organization.

Another type of acquisition is a reverse merger, a deal that enables a private organization to get publicly listed in a relatively short time period. A reverse merger occurs when a private organization which has strong prospects and is eager to raise financing buys a publicly listed shell organization, usually one with no business and limited assets. The private company reverse merges into the public limited organization, and together they become an entirely new public organization with tradable shares.

Creation of synergy by M&A

Regardless of their category or structure, all M&A have one common goal. They are all meant to create synergy that makes the value of the combined organization greater than the sum of the two parts. The success of a merger or acquisition depends on whether this synergy is achieved.

There are several reasons for M&A. These are (i) financial synergy for lower cost of capital, (ii) improving the performance of the organization and accelerate its growth, (iii) economies of scale, (iv) diversification of the organization for higher growth products or markets, (v) increasing of the market share and positioning giving broader market access, (vi) strategic realignment and technological change, (vii) considerations of taxes, (viii) under-valued target, and (ix) diversification of risk

M&A creates synergy which allows for enhanced cost efficiencies. The synergy value can be seen through the higher revenues, lowering of expenses, or the lowering of overall cost of capital. By M&A the organization hopes to benefit from the following.

- M&A results into improved sales revenues to employee’s ratio since employees? rationalization go along with M&A. The employee’s rationalization has also its impact on the wage bill of the organization.

- Economy of scale – Since in all the activities of the organization, there is an increase in the volume, the organization gets benefit of the economy of scale. As an example, M&A translates into improved purchasing power for the organization to buy equipment or office supplies i.e. when placing larger orders; organization has a greater ability to negotiate prices with its suppliers.

- Acquiring new technology – To stay competitive, the organization is required to stay on top of technological developments and their applications. Through M&A the organization enhances its technologies and maintains or develops a competitive edge.

- M&A helps the organization to improve its market reach and industry visibility. It helps the organization to reach new markets and grow revenues and earnings and to expand its marketing and distribution, giving it new sales opportunities. M&A also helps the organization to improve its standing in the investment community so that it can often have an easier time raising capital.

Role of valuation in M&A

The organization which is aiming to take over another organization, must determine whether the acquisition is going to be beneficial to it. In order to do so, it has to find out the real worth of the organization which is to be taken over. Naturally, both sides of an M&A deal always have different ideas about the worth of a target organization. The seller will tend to value the target organization at as high a price as possible, while the buyer always tries to value the target organization at the lowest price. However there are many legitimate methods to value organizations. The most common method is to look at comparable organization in the industry. Generally the following methods and tools are used for the assessment of a target organization.

- Comparative ratios – There are several comparative metrics which can be used for determining the value of the target organization to be taken over. Out of these two are very popular. The first is the ?price-earning? (P/E) ratio. With the use of P/E ratio, the organization which is taking over makes an offer that is a multiple of the earnings of the target organization. Looking at the P/E ratio for all the stocks within the same industry group provides a good guidance for the value of the target organization. The second is the ration of ?enterprise value to sales? (EV/sales) ratio. With this ratio, the organization which is taking over makes an offer makes an offer which is the multiple of the revenues. Again, the taking over organization is to be aware of the EV/sales ratios of other organizations in the industry.

- Replacement cost – In a few cases, M&A are based on the cost of replacing the target organization. In its simplest form, the replacement cost can be the sum of all its equipment and employees? However, this method of establishing a price certainly does not make much sense in a service industry where the key assets are employees and ideas which are hard to value and develop.

- Discounted cash flow (DCF) ?- DCF is a key valuation tool in M&A. DCF analysis determines the organization’s current value according to its estimated future cash flows. Forecasted free cash flows (net income + depreciation/amortization – capital expenditures – change in working capital) are discounted to a present value using the organization’s weighted average costs of capital (WACC). Normally DCF is tricky valuation tool, but only a few tools can rival this valuation method.

Normally the organization which is taking over usually pays a substantial premium on the stock market value of the organization to be taken over. The justification for doing so nearly always boils down to the notion of synergy which a merger benefits shareholders, when the taking over organization?s post-merger share price increases by the value of potential synergy.

It is unlikely for rational sellers to sell if they are benefitted more by not selling. This means that the buyers are required to pay a premium if they hope to acquire the target organization, regardless of what pre-merger valuation points to them. For sellers, this premium represents the organization?s future prospects. For buyers, the premium represents part of the post-merger synergy which they expect can be achieved. The following equation offers a good way to think about synergy and how to determine whether a deal makes sense. The equation is usually solved for the minimum required synergy.

(Pre- merger value of both organizations + synergy)/ Post merger number of shares = Pre-merger stock price.

In other words, the success of a merger is measured by whether the value of the organization taking over is enhanced by the action.

Stages involved in M&A

The following are the stages which are involved in M&A.

- Pre-acquisition review ? It is the first stage and includes self-assessment of the acquiring organization with regards to the need for M&A, ascertain the valuation (undervalued is the key) and chalk out the growth plan through the target.

- Search and screen targets – This is the second stage and includes searching for the organizations which are possible and appropriate to be taken over. The process includes mainly the scanning for a good strategic fit for the acquiring organization.

- Investigate and valuation of the target – It is the third stage. Once the appropriate organization is shortlisted through primary screening, detailed analysis of the target organization is required to be done. This activity is also known as ?due diligence?.

- Acquire the target through negotiations – The fourth stage consists of the start of the negotiations and to arrive at a consensus to achieve a negotiated M&A. This brings both the organizations to agree mutually to the deal.

- Post-merger integration – It is the fifth and the last stage in M&A. If all the first four stages fall in place, then there is a formal announcement of the agreement of merger by both the participating organization and after this the activities for the integration of the two organizations starts.

Reasons for the failure of M&A

The following are the likely reasons for the failure of M&A.

- Poor strategic fit – There exist a wide difference in the objectives and strategies of the organization.

- Poorly managed Integration – Integration is often poorly managed without the planning and proper design. This leads to failure in the implementation of the M&A.

- Incomplete due diligence – Inadequate or incomplete due diligence often leads to the failure of M&A as it is the core of the entire strategy.

- Overly optimistic – Too optimistic projections about the target organization leads to bad decisions and failure of the M&A.

Leave a Comment