Inventory Management and Control

Inventory Management and Control

In an organization there are stock of finished products, semi finished products, in process materials raw materials, spare parts, operating parts, fuels, and consumables. The collective name of these entire items is inventory.

Inventory occupies the most strategic position in the structure of working capital of the organization. It constitutes the largest component of current asset. The turnover of working capital is largely dependent on the turnover of inventory. It is therefore quite natural that inventory which helps in the maximization of profit occupies the most significant place among current assets.

The maintenance of inventory means blocking of funds and so it involves the interest and opportunity cost to the organization. The inventory cost is not only interest on stocks but also cost of store building for storage, insurance and obsolesce. Hence it is necessary that a great emphasis is placed on inventory management and control. The primary objectives of the management and control of inventory are as given below.

- To minimize the possibility of disruption in the production schedule for want of raw materials, consumables, spares and other stores items.

- To keep down the capital investment in inventories.

- To ensure sufficient stock of semi finished products so that there is no disruption in the production schedule.

- To ensure adequate stock of finished product to meet the delivery requirement of the customer.

It is essential to have only the necessary inventories. Excessive inventory is an idle resource which is a matter of concern. The investment in inventories is to be just sufficient and is to be at the optimum level. The major dangers of excessive inventories include the unnecessary tie up of the organizational funds, excessive carrying cost, and the risk of liquidity.

The excessive level of inventories consumes the funds of the organization, which cannot be used for any other purpose and thus involves an opportunity cost. The carrying cost, such as the cost of shortage, handling, insurance, recording, and inspection, are also increased in proportion to the volume of inventories. This cost will impair the organizational profitability further.

Management of the inventory is a daunting and difficult task and consists of supervision of supply, storage, tracking and accessibility of inventory items in order to ensure that there is an adequate availability of these items without over availability or under availability.

Like any other management process, management of inventory control also consists of a set of policies and operating procedures that are designed to maximize the use of inventory, so that there remains the least amount of inventory investment. It is normally done through stock control which shows how much stock of an item the organization is having any one time, and how to keep a track of the changing stock of the item. Stock control applies to every item and covers stock at every stage of the production process, from purchase and delivery to using and reordering and receiving of the item.

Efficient stock control helps the organization to have the right amount of stock in the right place at the right time. It ensures that capital is not tied up unnecessarily, and protects production if problems arise with the supply chain.

It is essential to have necessary inventories. Excessive inventory is an idle resource of the organization while a low level of inventories may result in frequent interruptions in the production schedule resulting in under utilization of capacity and lower sales. Both of such situations must be avoided. The investment in inventories is to be just sufficient to the optimum level.

The aim of inventory management thus is to avoid both the excessive as well as insufficient inventory and also to maintain adequate inventory so that the organizational operations can be run in a normal way. The effective inventory management has the following features.

- Maintenance of sufficient stock of materials to take care of the requirement during the period of short supply.

- To ensure a continuous supply of materials to the production departments for facilitating uninterrupted production.

- To minimize the carrying cost of the materials.

- Maintenance of sufficient stock of finished goods for smooth sales operations.

- To protect the inventory against deterioration, obsolescence and unauthorized use.

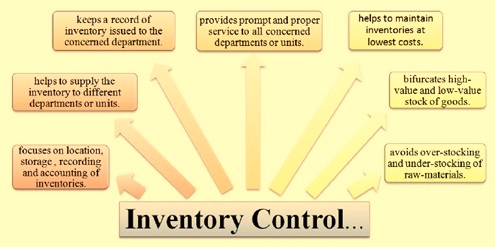

Inventory management must strike a balance between too much inventory and too little inventory. The efficient management and effective control of inventories help in achieving better operational results and reducing investment in working capital. It has a significant influence on the profitability of the organization. Main features of inventory control are given in Fig 1.

Fig 1 Features of inventory control

Inventory management and control techniques

The inventory management and control techniques are important due to the following reasons.

- A mismanaged inventory can lead to an unnecessary increase in the working capital. The excess funds can be fruitfully directed to fuel the organizational growth initiatives or research and development efforts.

- Effective inventory management leads to low storage costs, which in turn leads to an increase in the organizational profits. If the organization is able to manage the inventory well and is able to reduce the quantities that need to be stored, then the organization requires not only less storage space, but it also leads to lower store operational costs.

- It can help to satisfy the customers by providing them with the products they need in the swiftest manner. Poor inventory management leads to lower availability of the products and higher delivery time. Hence, for the sake of high customer satisfaction the organization needs to manage the inventory well.

- Item stored in inventory over a long period may spoil. This leads to unnecessary increase in the operational costs. Proper inventory management can help reduce these costs greatly.

- If the organization has inventories scattered in various locations, it need to have a proper system to manage these inventories on the basis of demand and supply. Inventory management techniques can help the organization go a long way in managing multiple inventories.

There are several techniques for inventories management and control. Some of them are described below.

- ABC inventory control technique – It is based on the principle that a small portion of the items may typically represent the bulk of money value of the total inventory used in the production process, while a relatively large number of items may from a small part of the money value of stores. Under this method, the inventory is classified into three categories, such as A, B and C. These categories are based upon the inventory value and cost significance. Also, the number of items and values of each category are expressed as a percentage of the total. Items of high value and small in number are termed as ‘A’, items of moderate value and moderate in number are termed as ‘B’, and items of small in value and large in number are termed as ‘C’. Group ‘A’ items need closer control while for group ‘C’ items control can be relaxed. However sufficient safety stock of group ‘C’ items is required to be ensured.

- VED analysis – It consists of classifying the inventory items as vital (V), essential (E), and desirable (D). Vital items are those items for want of which the production comes to a complete halt. These are normally long lead items and usually proprietary items. Essential items are those items whose stock outs cost is very high while the desirable group are those items which does not cause serious production problems since alternatives can be used in case of stock out of these items.

- SDE analysis – Under this analysis, items are classified as scarce (S), difficult (D), and easy (E). This classification is done to decide the purchasing strategies. Scarce items are those which are short in supply, imported or canalized through government agencies. Difficult items are those which are available indigenously but are not easy to procure while the easy items are those which are which are readily available in the market.

- GOLF analysis – It is based on nature of suppliers which determine quality, lead time, terms of payment, continuity or otherwise of supply and administrative work involved. The analysis classifies the items into 4 groups. G group covers those items which are to be procured from the government agencies. Transactions with this category of items involve long lead time and payments in advance or against delivery. O group covers those items which are procured the open market normally from private agencies. Transactions with this category of items involve moderate delivery time and usually with the availability of credit. L group contains those items which are bought from local suppliers. The items bought from these suppliers are usually cash purchased or purchased on blanket orders. F group contains those items which are purchased from foreign suppliers. Purchase of these items involve a lot of administrative work, require opening letter of credit, and require making of arrangement for shipping & port clearance.

- SOS analysis – Under this classification, the items are classified as seasonable (S) or off seasonable (OS). Seasonable items are those items which are not available during off season and they are to be procured and stored during the season. Examples are sand, rice husk etc. Off seasonable items are those items which are available in the off season but with lower availability and higher costs.

- MNG analysis – This analysis is based on stock turnover rate and it classifies the items into M (moving items), N (non moving items), and (ghost items). Moving items are items consumed from time to time. Non-moving items are items not consumed in the last year while ghost items are those items which had nil balance, both in the beginning and at the end of the financial year. Ghost items are needed to be removed from the inventory list.

- FSN analysis – This analysis is based on consumption figures of the items. Under this analysis, inventory items are classified into three groups namely F (fast moving), S (slow moving), and N (non moving).

- AP (automatic procurement) items – AP items are those items where a minimum safety stock of items is necessary to be maintained for ensuring the smooth production. Once the stock falls below the safety level, automatic procurement action is requires for these items without any further approval.

- Economic order quantity (EOQ) – EOQ represents the most favorable quantity to be ordered each time fresh orders are placed. The quantity to be ordered is called economic order quantity because the purchase of this size of material is most economical. It is helpful to determine in advance as to how much should one buy when the stock level reaches the order level. If large quantities arc purchased, the carrying costs would be large. On the other hand, if small quantities are purchased at frequent intervals the ordering costs would be high. The economic order quantity is fixed at such a level so as to minimize the cost of ordering as well the cost of carrying the stock. It is the size of the order which produces the lowest cost of material ordered.

- Just in time – Just in time technique can be risky, especially if it is not implemented correctly, but if the organization can do it in a right way then it can be most rewarding. Just in time technique involves having item received in the organization just at the time when it is needed. It can be risky because there may be so many variables which may not be always perfectly predictable.

- FIFO principle – To avoid deterioration of the quality of inventory while it is under storage, it is necessary that he principle of FIFO (first in first out) is applied for inventory items in the stores.

Leave a Comment