Cost Control during Production

Cost Control during Production

The broad definition of costs is related to the economic resources necessary to accomplish work activities or to produce work outputs. Usually, costs are expressed in terms of units of currency. Therefore, costs are the amount of money representing the resources spent for the production of output. A resource is a physical entity that is required to be able to execute a certain operation. Resources can be e.g. machine and equipment, raw materials, utilities, tools, fuel and energy, but also operators and consumables. Outputs are the products and byproducts.

The success of an organization largely depends on the profit that it can realize. The profit is determined by the costs that are made and the extent to which these costs are recovered. Therefore, it is essential for the organization to know all the costs so that it is able to control them. Cost control is a managerial effort to attain cost goals within a particular environment. Cost control is not a specific program. Rather, it is a routine activity carried out continuously. Cost must be controlled; otherwise, there will be wastage and misappropriation. Cost control is an important activity for any efficient organization since it has a major impact on the profitability of the organization.

The costs throughout the entire organization are to be known to the management so that it can be used for the purpose of decision making. Therefore, it is necessary to integrate the cost information in the management process. For this a system is needed that can support the management with the cost data and hence in controlling the cost.

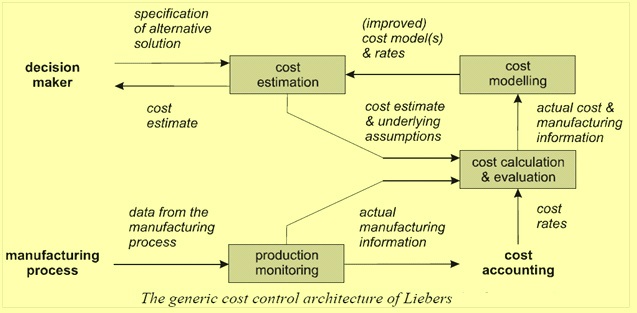

According to Liebers the cost control component can be broken into four functions namely cost estimation, production monitoring, cost calculation and evaluation, and cost modeling. The functions of cost control and their input and output are shown in Fig 1.

Fig 1 Functions of cost control

Production cost control is built around and forms part of the operations of a producing organization. The main requirement for the calculation of production cost is the plant production and consumption data and statistics which are normally measured as part of the plant operation.

Cost control relies heavily on accounting techniques. Some of the key cost control techniques are responsibility accounting control system, standard costing, budgetary control and cost management ratios.

In any organization, major cost is incurred during the production process. Hence major attention of management is needed for control of production cost. The objective of production cost control is to develop a costing system that can provide cost information throughout the whole production process and that can be used for cost control. In order to be independent of the production environment, the costing system has to be based on real time process data.

Production cost is measured as ‘per unit of the product’. In those organizations where several intermediate products are produced before the production of final saleable product, production cost is measured for each intermediate product as ‘per unit of the intermediate product’.

The cost data are broken down and correlated with the factors that control their values. The cost data is useful for cost control if it is reliable, is based on the production and consumption data, and is related to the factors which affect the production cost.

Cost control is the regulation by executive action of the costs of operating a process or processes particularly where such action is guided by cost accounting. It is function, which makes sure that the process is performing as per plans and as intended. It is a widely accepted notion that the actual costs for each cost element should be within the budget.

During a production process the costs can be direct costs or indirect costs. Direct costs are those costs which are identified specifically and consistently with the product while the indirect costs are allocated to the product based on some assumptions.

Costs elements are usually fall into two categories. These are variable costs and fixed costs. Fixed costs and variable costs comprise total cost. Variable costs are those costs that vary depending on the production volume. These costs rise as production increases and fall as production decreases. Variable costs differ from fixed costs which tend to remain the same regardless of production output.

Mathematically, the relationship existing between volume of production and costs can be expressed by the following equations.

Unit cost = Variable cost per unit of product + Total fixed cost/ output

Production cost is based on the actual performance during production. Production cost control is done by comparison of actual cost with the standard cost, budget cost or aimed cost. The standard cost is calculated based on the standard parameters of the production process. These costs are made on the basis of process capabilities i.e. consumption norms as well as fixed charges at cent percent capacity utilization level. The budget cost is calculated based on the budgeted parameters for the production process while the aimed cost is calculated based on the desired process parameters. All the three costs uses predetermined per unit costs and are important for the control of the production cost.

For calculating the production cost, it is usually broken down in various components. Monitoring of each cost component is important to satisfy that all the areas during the production of the product are functioning normally and also to take necessary actions in case a cost component has gone out of control. Further those components whose contribution is higher in the production cost need closer monitoring. The important variable cost components for production cost are as follows.

- Raw material cost – Normally it is the major component of the production cost. Raw material cost is dependent on quality of raw material, yield of product, handling loss, moisture content of the raw material, and wastages associated with the use of the raw material etc. Raw material cost is also influenced by the level of waste recycling.

- Fuel and energy – This is also a major component of the production cost. Fuel and energy cost is dependent on the technology employed for the production, type and quality of fuel and energy under use, recovery of the waste energy from the process, and handling losses etc.

- Power cost – Power cost also contributes substantially to the production cost. Power cost is dependent on the quality of power, line losses, idle running of the motors as well as the process productivity.

- Maintenance cost – It is greatly influenced by the type of maintenance being employed for the plant and equipment. Other major component of the maintenance cost is the inventory cost for the spares parts. Maintenance cost is also influenced by the extent of outsourcing of the maintenance activity.

- Utility cost – This is the cost incurred due to the consumption of water, utility gases, compressed air, and process steam etc. This cost contributes substantially to the production cost.

- Manpower costs – Manpower costs varies with the level of automation as well as the man productivity. Man productivity in turn is dependent on the education and training of the work force as well as the extent of supervision needed.

- Inspection cost – Cost of inspection is normally not the major production cost unless and until during inspection it is noticed that the production process have been out of control resulting into either diversion of the product or rejection of the product.

Fixed cost component of the production cost is highly dependent on the production level. Higher the production lower is the fixed cost component in the production cost. Important fixed cost components of the production cost are given below.

- Over heads – In production costs there are usually two types of overhead namely works overheads and administrative overheads. Works overheads are for the fixed expenditure directly related to production departments while the administrative overheads are due those fixed expenditure which are outside the production departments.

- Interest on working capital – This is the works overhead and depends on the amount of working capital employed as well interest rate on the working capital.

- Interest on capital

- Depreciation

Production cost excluding interest on capital and depreciation is known as works cost.

An important aspect of cost management is the variance analysis. Variance analysis can be done between actual cost and standard cost or budget cost. Variation analysis breaks down the variation in the costs into various components such as volume variation, material cost variation, and manpower cost variation etc. This helps the management to understand which factor is affecting most for the cost variation with the planned cost and in turn helps in taking appropriate corrective action to correct the situation.

Leave a Comment